Why Waiting for Lower Mortgage Rates Could Actually Cost You More

Let’s have some real talk for a minute.

I know mortgage rates have a lot of buyers nervous right now — especially my military families relocating to San Antonio, first-time buyers, and families trying to figure out if now is “the right time” to move.

Every time rates move up a little, I hear the same thing:

“We’re just going to wait until rates drop.”

And I completely understand why people feel that way.

But here’s what many buyers don’t realize…

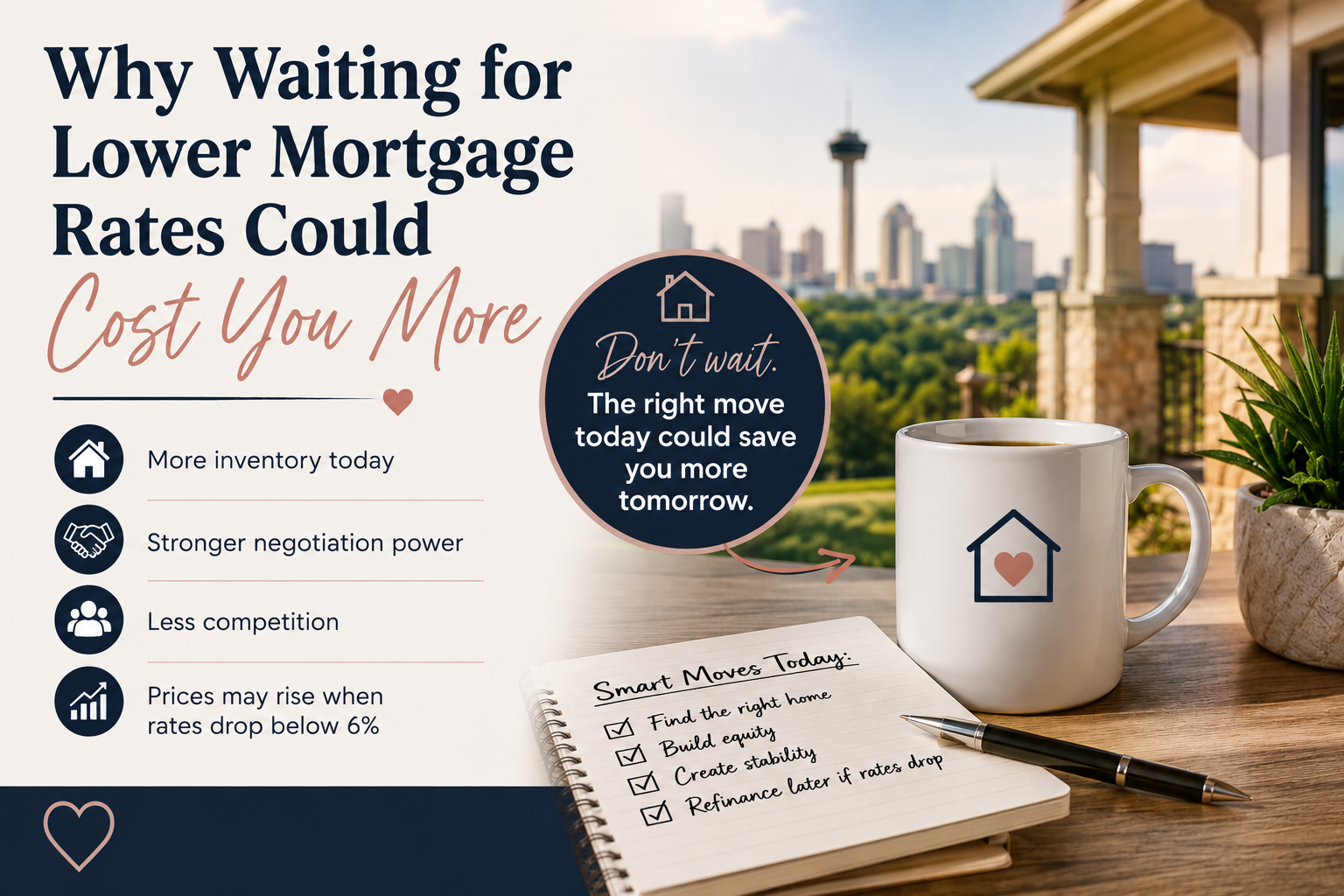

Waiting for that “perfect” interest rate could actually end up costing you more in the long run.

The Reality About Rates

Experts are already starting to project that mortgage rates could dip below 6% sometime in 2026.

Sounds amazing, right?

The problem is… you are not the only person waiting for that moment.

According to the National Association of Realtors, millions of buyers who have been sitting on the sidelines are expected to jump back into the market once rates hit that psychological “sweet spot.”

And when that happens?

More buyers = more competition.

More competition = rising home prices, multiple offers, and less negotiating power.

Right now, buyers still have opportunities that were almost impossible to find a few years ago:

- More inventory

- More seller concessions

- Better negotiation leverage

- More time to make decisions

- Less bidding war pressure

Those advantages start disappearing the moment the market heats back up.

The Difference Might Be Smaller Than You Think

Here’s the part most people don’t calculate.

On a $400,000 mortgage, the payment difference between today’s rates and a rate just under 6% is often around $50-ish per month.

That’s it.

Meanwhile, if home prices increase because thousands of buyers rush back into the market at the same time, you could end up paying significantly more for the house itself.

So while everyone is waiting for rates to fall…

Home prices may quietly keep climbing.

Especially for Military Relocation Families…

This is something I talk about with my PCS and relocation clients all the time.

When you’re relocating to San Antonio, timing matters — but so does opportunity.

Sometimes the best move is securing the right home, in the right location, with the right terms NOW… instead of trying to perfectly time the market later.

Because the truth is:

You can refinance a rate later.

You cannot go back and buy the house after prices rise or competition increases.

The Bottom Line

Don’t let today’s rates scare you away from building wealth, creating stability, or finding the right home for your family.

The buyers who win in real estate are usually the ones who make smart long-term decisions — not the ones waiting for perfect market conditions that may never come.

If you’re considering relocating to San Antonio, buying your first home, or using your VA loan benefits, I’d love to help you create a TaylorMade game plan that makes sense for YOUR situation.

Because real estate isn’t one-size-fits-all.

It should be TaylorMade to fit YOUR needs.

Categories

Recent Posts